A low interest credit card is a most sorted best option for you to save money on making monthly payments through your credit card and especially for those cardholders who transfer their outstanding balance from one month to another month. There are few cards that come with 0 % introductory APR and some with low interest . Always choosing the right credit card is not as easy . So here is the list of the Best Low Interest Credit Cards To Save Money This Year .

Best Low Interest Credit Cards To Save Money This Year

Here is the list of the Best Low Interest Credit Cards with 0% APR and low APR Interest Credit cards .

- Chase Slate

- BBVA Compass Visa Signature

- PenFed Promise Visa Card

- Citi Diamond Preferred Card

- Discover it chrome card

- Citi Simplicity Card

- Discover it

- Barclaycard Ring Mastercard

- Chase Freedom

- HDFC Infinia Credit Card

- Citibank Rewards Credit Card

- First Citizen Citibank Titanium Credit Card

- ICICI Bank Instant Platinum Credit Card

- Kotak Velocity Platinum Credit Card

- Jet Airways Citibank Titanium Credit Card

- SBI Advantage Platinum Credit Card

- ICICI Bank Instant Gold Credit Card

- SBI Advantage Plus Credit Card

- TATA Empower Credit Card

So now let’s take a detailed look on each of the Best Low Interest Credit Cards .

Read Also : Quickly increase credit score in just 12 months -Easiest hack

Read Also : Purchase without credit card top hacks

Read Also : Pros and cons of credit cards – All the Hidden Facts on Credit cards

Read Also : Credit Card Debt Myths – Top 8

Chase Slate

Chase Slate is one of the Best Low Interest Credit Cards .

- $0 introductory balance transfer fee if you transfer during the first 60 days of your account opening. You have to pay 0% Introductory APR for almost 15 months on purchases and balance transfers. You can view every month updates to your FICO® Score and it will also tell you the reasons behind your score for free.

- No Penalty APR – even if you Pay late it won’t raise your interest rate and the best part is $0 Annual Fee.

BBVA Compass Visa Signature

This is one of Best Low Interest Credit Cards that is preferred for its features like –

- Visa Zero Liability

- No annual fee charged with the Visa Signature card.

- You can simply enjoy VIP Entertainment by special advance entrance to major sporting events, Hollywood blockbuster screenings, Broadway shows and more.

- You can simply Save your time with 24-hour complimentary Concierge service that can assist you with travel plans, dining reservations and further.

- Enjoy special offers and receive complimentary discounts as well as travel upgrades along with discounts at premium retailers.

Read Also : Credit Card Debt Pay Off- 5 Things to Consider About Debt Pay Off

Read Also : Student Credit Card Alternatives – Better than Credit Card

PenFed Promise Visa Card

- No balance transfer

- No cash advance

- No late fee or penalty APR

Citi Diamond Preferred Card

if you face problem while paying your balance then you can definitely register for citi diamond preferred card as it also offers some additional perks like 0% intro APR for 21 months on balance transfer and purchases. the cardholder will also be able to buy exclusive tickets and pre-sale tickets to event with citi private pass.

Discover it chrome card

the cardholder will get $20 cash back if you score GPA 3.0 or above till 5 years in your school. they can also earn 2% cash back at gas as well as restaurants on up to $1,000 quarterly. 1% cash back in addition on all other purchases. all the cash back that the cardholder has earned will be matched at the end of the first year.

Citi Simplicity Card

- You can take advantage of a low intro APR on credit card balance transfers and purchases. In addition, keep it simple with no late fees, no penalty rate and no annual fee ever.

- 0% Intro APR is charged for 18 months from date you open your account on purchases and 0% Intro APR for 18 months from date you make the first transfer on balance transfers.

- Balance Transfer Fee is either $5 or 3% of the amount that you have to pay of each credit card balance transfer, whichever is greater.

- No Annual Fee to be charged.

Read Also : Types of Insurance You Must Know to Secure Life

Barclaycard Ring Mastercard

The cardholder has to pay no annual fee which means $0 annual fee as well as $0 as balance transfer fee.

24% variable APR for purchases as well as balance transfer and cash is charged that may vary with the market based prime rate.

HDFC Infinia Credit Card

The HDFC provides Infinia credit Card charges very low interest rate as well as charge cash advance amount as low as 1.99%. Although, the joining fee and renewal is high, at higher amount like 30,000 and little less on lesser amounts for e.g. 10,000. HDFC Infinia is the best low interest credit card. It doesn’t have any limit of spending money in advance. The cardholders also get rewarded with 5 points on every transaction that they make worth Rs.150.

Read Also : Improve Credit Score For Getting Loan Approval – CIBIL Score Detailed

Citibank Rewards Credit Card

Citibank Rewards Credit Card offers zero fees at the point of registration. It charges 3.15% interest rate along with 2% cash advance fee. You can enjoy up to 10X Rewards, every time you go for shopping at your favourite store.

First Citizen Citibank Titanium Credit Card

You don’t have to pay and joining or renewal fee. Citibank First Citizen Titanium card charges 3% of interest rate and 2% as a cash advance fee. First citizen Citibank titanium Credit cardholders can avail reward points or gift vouchers as well as other benefits only at some of the stores.

ICICI Bank Instant Platinum Credit Card

The ICICI Bank Instant Platinum Credit Card charges just 2.49% of interest rate and also 2.49% as cash advance fee. You can join for free and also renew your card for free. The ICICI Bank Instant Platinum Credit Cardholders can avail interest-free credit for up to 48 days while making payment through your card.

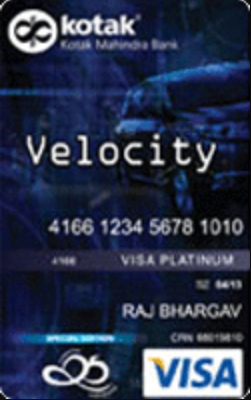

Kotak Velocity Platinum Credit Card

- The Kotak Velocity Platinum Credit Card is the best low interest credit card as one has to pay very low interest rate which is 3.10% that has to pay every month.

- The best part is that the Joining fee which of almost Rs.499, is waived off especially just for the kotak velocity platinum credit cardholders.

- But you may have to pay Rs.499 at the time of renewing your card as renewal fee, whereas the cardholder has to also pay 2.5% in favour of advance fee.

- This is also recommended as the best low interest credit card as it offers 2.5% fuel extra discount in all petrol pumps in all over in India. Hurry and register today.

Jet Airways Citibank Titanium Credit Card

Citibank provides the Jet Airways Titanium Credit Card which known as the best low interest credit card. The cardholder has to pay 2.5% of interest rate for every month as well as 2% as cash advance fee. The cardholder can also earn double and redeem JPMiles on Jet Airways tickets. One can earn up to 1000 JPMiles while using this card for the first time every year.

SBI Advantage Platinum Credit Card

- 99% of interest rate every month

- 5% as a cash advance fee.

- 2999 as joining fee and renewal fee.

- The best part is that the cardholder can earn and redeem almost 5X Cash Points while shopping from their favourite apparel store, Departmental Stores or at any fine – Dine restaurant or else even spending in abroad.

ICICI Bank Instant Gold Credit Card

- 49% interest rate per month

- 49% cash advance fee

- ICICI Bank Instant Gold Credit Card is the best low interest rate credit card.

- No joining fee

- No renewal fee

SBI Advantage Plus Credit Card

we recommend this as the best credit card as is charges very less joining fee and just Rs.500 as renewal fee from the cardholder. 1.99% per month interest rate and 2.5% cash advance fee to be charged every month. it also includes a credit free time of 50 days.

TATA Empower Credit Card

Zero joining and renewal fee yes you heard it correctly. The TATA Empower Credit Card asks you to pay very low interest rate of 3.35% and 2.50% every month. The cardholders can simply benefit up to 4% value back at various Tata stores and products as well as their partner stores. Thus this is recommended as one of the Best Low Interest Credit Cards .

So hope we have given an exclusive list of Best Low Interest Credit Cards or the 0 % APR Cards that you can choose the ideal credit card that matches your need .